An elementary school teacher, seeking to manage her family’s healthcare expenses, opted for a health insurance plan with a lower monthly premium. However, the decision soon revealed a critical gap in her understanding of the financial implications, particularly concerning the concept of a deductible. "Once I got the insurance card, I compared our old plan to our new plan, and that’s when I really got worried, because I didn’t really understand what a deductible was," shared Madison Burgess, a 31-year-old educator from San Diego. "It got me thinking, how do I use this insurance?" This sentiment underscores a growing concern for many Americans who find themselves navigating the complexities of high-deductible health plans (HDHPs) in an increasingly challenging healthcare landscape.

The expiration of enhanced federal subsidies at the close of 2025 has led to a significant increase in expected monthly rates for individuals purchasing health insurance through state and federal exchanges. In response, a substantial number of consumers have shifted towards HDHPs, attracted by their lower upfront monthly payments. However, this cost-saving measure often comes with a trade-off: considerably higher out-of-pocket expenses when medical services are required.

The prevalence of HDHPs has surged in recent years. Data from 2023 indicates that 30% of individuals obtaining insurance through their employers were enrolled in an HDHP, a stark increase from a mere 4% in 2006. This trend reflects a broader shift in healthcare financing, where individuals are increasingly shouldering a larger portion of their medical costs.

Burgess’s experience exemplifies the common pitfalls associated with selecting an HDHP without a thorough understanding of its terms. As a teacher, she receives health insurance through her employer. However, when she explored adding her husband to her existing plan, the cost proved prohibitive. This prompted her to search for more affordable alternatives on the health insurance exchange. The sheer volume of plan options and the intricate insurance jargon presented a daunting challenge, making it difficult to ascertain her family’s potential financial liability should her husband require medical care. "I didn’t know what a deductible was, so I just went with what was cheap, and now I have regret," she admitted.

Under her husband’s new coverage, most medical services will not be covered by insurance until the family has paid $5,800 in out-of-pocket medical expenses. This substantial sum represents the deductible, a crucial component of HDHPs that requires policyholders to pay a significant amount of medical bills before their insurance coverage begins to share the financial burden. Burgess’s realization highlights a common knowledge deficit regarding the fundamental mechanics of these plans.

Understanding the Pillars of High-Deductible Health Plans

To better comprehend the implications of HDHPs, it’s essential to define their core components:

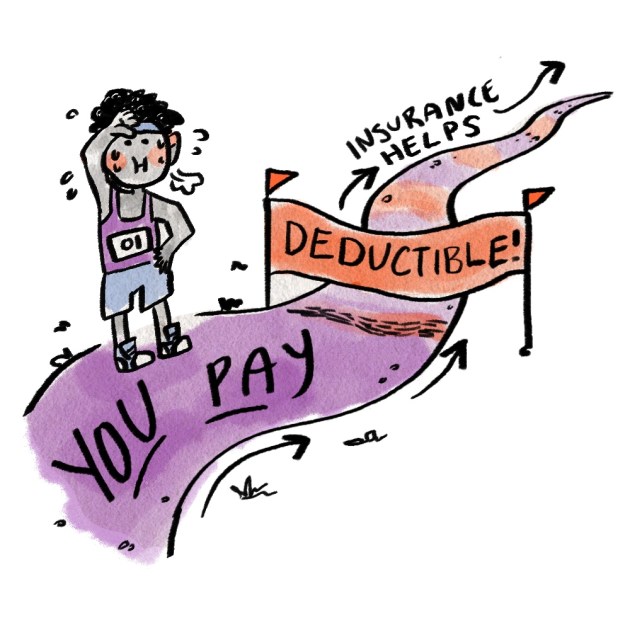

- Deductible: This is the fixed amount that a policyholder must pay out-of-pocket for covered healthcare services before their insurance plan starts to contribute financially. For example, if an individual has a $5,800 deductible, they will be responsible for paying the first $5,800 of their medical bills.

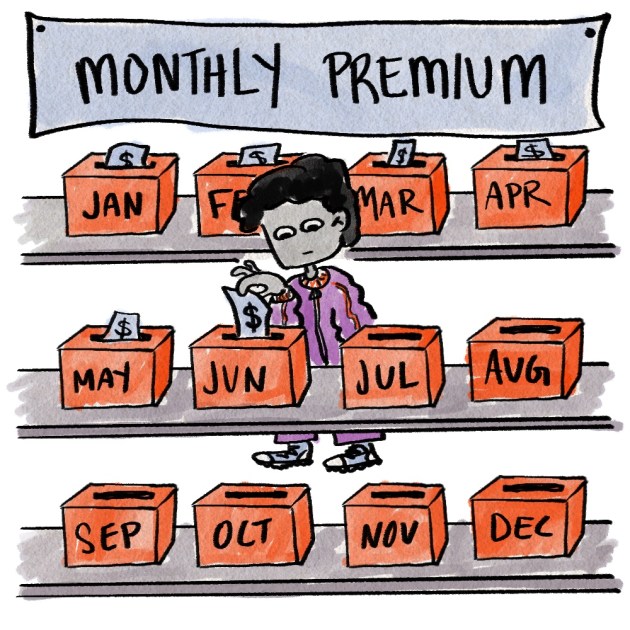

- Premium: This is the regular payment made by the policyholder to the insurance company to maintain their health insurance coverage. Premiums are typically paid monthly, and HDHPs generally offer lower monthly premiums compared to plans with lower deductibles.

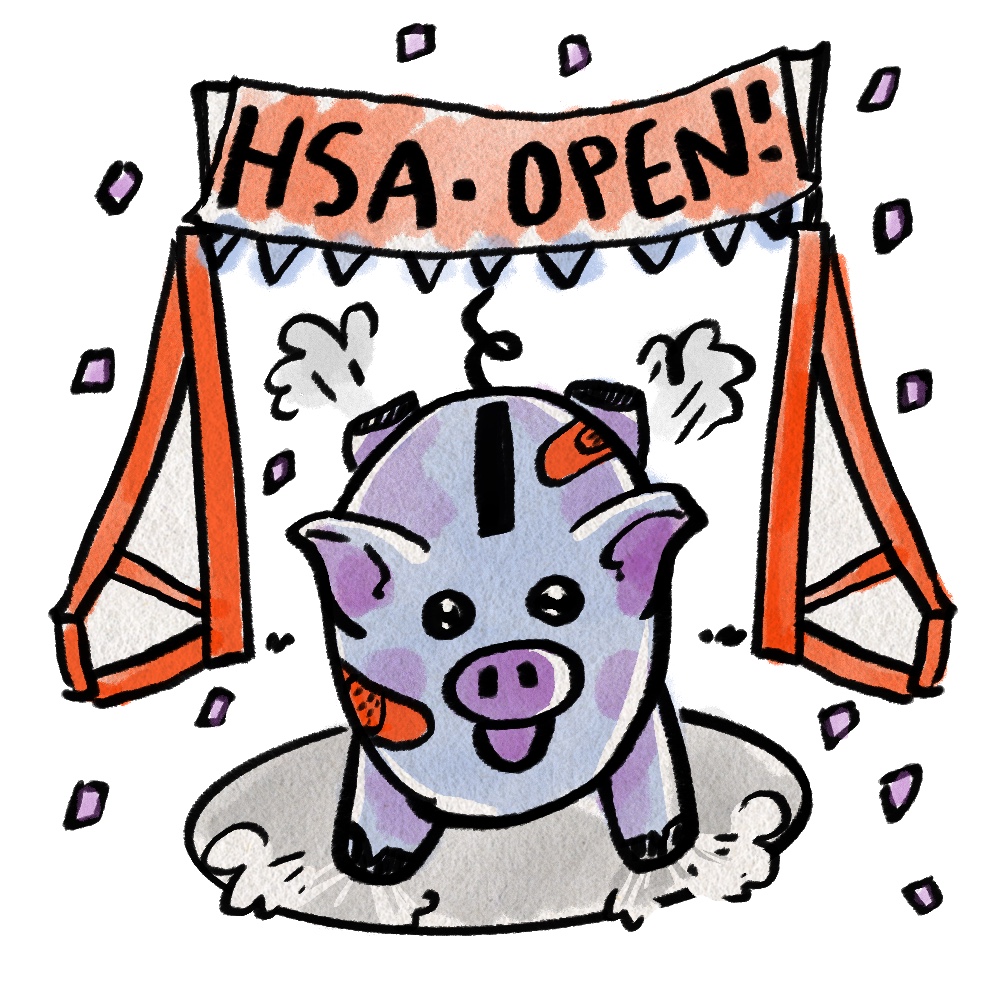

The allure of lower monthly premiums in HDHPs, such as the bronze plan Burgess selected, can overshadow the potential for substantial out-of-pocket expenditures. This was precisely Burgess’s predicament; she was unaware that a Health Savings Account (HSA) could have been a viable option to help manage these upfront costs. HSAs are designed to work in conjunction with HDHPs, allowing individuals to set aside pre-tax money to cover qualified medical expenses.

Many individuals, like Burgess, find themselves unprepared for the financial demands of a high deductible. The prospect of accumulating thousands of dollars for unexpected medical bills often competes with more immediate financial priorities such as rent, utilities, and everyday living expenses. The common tendency is to prioritize saving for predictable emergencies like car repairs or household maintenance rather than for potentially less frequent, albeit significant, medical needs.

Strategies for Navigating HDHPs and Managing Out-of-Pocket Costs

For consumers who have opted for more affordable coverage this year and are now facing the reality of a high deductible, several strategies can help mitigate the financial strain.

1. Unlocking the Potential of Health Savings Accounts (HSAs)

A significant number of individuals enrolled in bronze or catastrophic health plans may be eligible to open a Health Savings Account (HSA) without realizing it. An HSA functions as a medical savings vehicle, offering considerable tax advantages. Contributions made to an HSA are tax-deductible, effectively lowering an individual’s taxable income. Furthermore, the funds within the HSA grow tax-free, and withdrawals for qualified medical expenses are also exempt from taxation. This "triple tax advantage" makes HSAs a powerful tool for managing healthcare costs.

HSAs can be used to cover a wide array of medical expenses, including doctor’s visits, prescription medications, dental care, vision care, and even over-the-counter items like bandages, tampons, and sunscreen. It is important to note that HSA funds are generally not permitted for monthly insurance premiums, with some exceptions for COBRA premiums or long-term care insurance. A key benefit of HSAs is that the funds belong to the account holder, regardless of employment status or changes in health insurance plans. This portability distinguishes HSAs from Flexible Spending Accounts (FSAs), which are typically employer-sponsored, have an annual "use-it-or-lose-it" provision, and the funds are forfeited upon leaving employment.

2. Opening and Utilizing a Health Savings Account

Establishing an HSA is a straightforward process, typically initiated through a bank or other financial institution. Upon opening an account, the individual receives a debit card for convenient access to the HSA funds for medical purchases. Eligibility for opening an HSA is tied to enrollment in a High Deductible Health Plan (HDHP) that meets specific IRS criteria. Individuals can open an HSA at any point during the year, provided they are enrolled in an eligible plan. When selecting a financial institution for an HSA, consumers are advised to compare fees and explore various options. Employers may mandate the use of a specific HSA provider for those enrolled in employer-sponsored HDHPs.

While the appeal of an HSA is evident, many individuals perceive themselves as unable to allocate funds due to competing financial obligations. However, the flexibility of HSAs allows for contributions of any amount, even a few dollars a month, to begin building a financial cushion. The Internal Revenue Service (IRS) sets annual contribution limits for HSAs. For 2026, these limits are projected to be $4,400 for individuals and $8,750 for families. Within these limits, individuals have the autonomy to determine their contribution amount.

3. Leveraging No-Cost Preventive Services

A significant advantage of health insurance plans purchased through the Affordable Care Act (ACA) marketplaces is the mandatory coverage of certain preventive services at no cost to the patient, provided the services are rendered by an in-network provider. These essential services include vaccinations, annual physicals, and screenings for various cancers. This provision encourages early detection and intervention, potentially averting more serious and costly health issues down the line.

Beyond these mandated preventive services, understanding the cost variations for different types of medical care can empower consumers to make informed decisions that align with both their health needs and their financial capacity. For instance, some plans offer lower costs for telehealth consultations compared to in-person visits with a primary care physician. Detailed information regarding these cost differentials can typically be found in the plan’s Summary of Benefits and Coverage (SBC).

4. Strategic Timing of Medical Care

A crucial aspect of managing deductibles is understanding that they typically reset at the beginning of each calendar year, on January 1st. For individuals who discover a medical condition requiring ongoing treatment or anticipate needing elective procedures, strategically scheduling these services early in the year can be financially advantageous. By meeting the deductible sooner, policyholders can benefit from their insurance coverage kicking in for the remainder of the year, thereby reducing subsequent out-of-pocket expenses. Caitlin Donovan, a senior director at the Patient Advocate Foundation, emphasizes the importance of this timing, noting that "meeting your deductible sooner can make the rest of the year significantly cheaper."

5. The Option of Paying Cash for Medical Services

In certain situations, paying for medical services in cash directly to providers may result in lower costs than utilizing insurance, especially for individuals with very high deductibles who may not anticipate meeting them. Providers, including hospitals, clinics, and individual practitioners, may offer discounted cash prices. Consumers have the legal right to request an itemized estimate of all anticipated medical service costs before receiving care. This "Good Faith Estimate" allows for a comparison between the cash price and the anticipated cost through insurance. If opting for a cash payment, it is essential to settle the bill at the time of service, before the charges are submitted to the insurance company. While paying cash can lead to immediate savings, it’s important to recognize that these payments typically do not count towards the annual deductible or out-of-pocket maximum. As Donovan advises, "If you don’t think you’re ever going to hit your deductible—you’re that young invincible, and your deductible is $10,000—negotiate the cash price."

6. Keeping ACA Marketplace Information Current

Individuals enrolled in ACA plans who receive premium subsidies need to be particularly diligent about updating their income information on the marketplace application. Failure to report changes in earnings—such as raises, new employment, or supplementary income—can lead to an unexpected tax liability at the end of the year. The IRS requires that advance premium tax credits (APTCs) accurately reflect an individual’s projected annual income. If actual income exceeds the projected amount, the excess subsidy must be repaid.

The remedy for this potential issue is straightforward: report any changes in income to the health insurance marketplace as they occur. This proactive approach can prevent a substantial tax bill. For instance, if an individual experiences an increase in income, stashing funds in an HSA can be beneficial, as HSA contributions are not counted towards taxable income. While a reported income increase might lead to higher monthly premiums if eligibility for a particular subsidy level changes, it is generally more financially prudent to pay slightly more in premiums throughout the year than to face a large, lump-sum tax payment. Donovan warns, "One of the biggest problems I see is someone is newly unemployed and they sign up for coverage, they say that they’re not making any money, and then eventually they get a job and don’t report it, and then they have this huge tax bill at the end." Regularly updating the marketplace profile can also reveal eligibility for Medicaid or other plans that offer more comprehensive coverage for medical bills.

The journey through the complexities of health insurance, particularly with the rise of high-deductible plans, necessitates a proactive and informed approach. By understanding the nuances of deductibles, premiums, and available savings vehicles like HSAs, consumers can better navigate the healthcare system and protect themselves from unexpected financial burdens. The increasing reliance on HDHPs underscores the critical need for greater transparency and consumer education within the healthcare marketplace.

{kind=link}